Digital Insurance faced problems in 2024 and was paved with difficulties. The brilliant illusion of immediate quotations, highly customized coverage, and 24/7 access. Shadows lie underneath the enticing exterior, raising questions about the very viability of digital protection. Consumers feel frightened about cybersecurity because of fraudulent schemes and data. On the other hand, the regulatory setting makes it impossible to enforce new laws since it resembles a convoluted maze. with innovation, leaving customers and insurers bewildered. Where is this digital odyssey’s travel map? A tech tsunami spearheaded by agile startups that rewrite the laws of the game surges upon the coast just as established giants cling to their thrones.

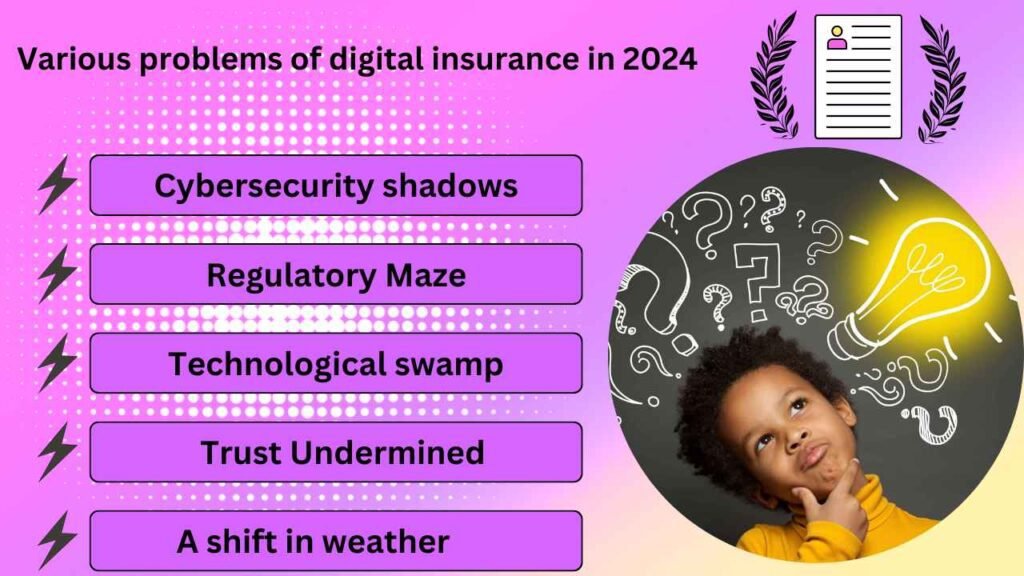

Various problems of digital insurance in 2024

In 2023, digital insurance’s dream of convenience collided with a harsh reality of hidden challenges. Cyberthreats cast shadows on data security, and complex regulations tangle the path forward and are disruptive. Tech waves threatened to topple traditional models. But the deepest cracks ran through trust, as anxieties about data privacy and opaque algorithms chipped away at the foundation. This is not just a quest for efficiency; it’s a fight for the future of our financial security. We must confront the darkness beneath the gleaming facade.

Cybersecurity shadows

In the gleaming halls of digital insurance, a chilling echo whispers – the threat of cybercrime. Data breaches slither through the code, pilfering identities and financial secrets. Malicious code dances in the shadows, weaving webs of deceit to drain bank accounts and expose vulnerabilities. Trust, the lifeblood of any insurance, shivers under the cold breath of these unseen threats.

Regulatory Maze

The digital insurance landscape races forward, while regulations struggle to keep pace, trapped in a tangled maze of bureaucracy. Confusing rules and evolving guidelines leave both insurers and consumers disoriented and unsure of the path forward. To emerge from this labyrinth, industry-wide collaboration is crucial. We need a clear roadmap, paved with comprehensive and adaptable regulations that foster innovation while safeguarding financial security.

Technological swamp

Traditional insurance giants face a rising tide—a tsunami of InsurTech startups wielding the power of disruptive technology. These nimble, tech-savvy players rewrite the rules of the game, offering personalized coverage and streamlined processes. To survive this wave, the old guard must embrace innovation, adapt their models, and ride the crest of the technological wave.

Trust Undermined

Under the sheen of convenience lies a deeper anxiety—the erosion of trust. Data privacy concerns gnaw at us, whispering fears of our most intimate details being exploited and misused. Opaque algorithms, operating in the black box of AI, fuel anxieties about unfair pricing and hidden biases. These are not mere inconveniences; they are fundamental challenges that threaten the very foundation of our digital safety net. We must confront these shadows lurking beneath the gleaming surface, for the future of our financial security depends on it.

A shift in weather

In 2024, digital insurance will confront significant challenges because of the ongoing shift in climate styles. The increasing frequency and severity of severe climate events, inclusive of hurricanes, wildfires, and floods, posed heightened risks to insured residences and belongings. Insurers needed to grapple with the growing variety of claims resulting from climate-related damages, leading to extended payouts and monetary lines on their operations. Furthermore, the evolving nature of climate dangers necessitated the model of coverage fashions and underwriting practices to correctly examine and price those dangers, ensuring the lengthy-term sustainability of digital insurance in a changing weather landscape.

Inflation as it relates

Chronic inflationary pressures in 2024 posed significant hurdles for virtual insurance providers. Medical inflation, in particular, has a significant influence on healthcare prices, increasing costs for medical health insurance rules and claims fees. Furthermore, larger financial inflationary tendencies influenced asset and liability coverage, as growing prices of building materials, labor, and property values prompted changes in insurance and pricing. To maintain profitability while also assuring affordability and enough protection for consumers, insurers have to negotiate those inflationary tendencies with caution.

Threat to belongings

Digital insurance faced mounting threats to property in 2024, exacerbated by climate change and the increasing frequency of severe climate events. Properties were increasingly more prone to harm from hurricanes, floods, wildfires, and other natural failures, leading to better coverage claims and asset losses. Insurers grappled with the desire to correctly examine and free belongings dangers while also promoting resilience and chance mitigation measures amongst policyholders. Furthermore, the emergence of cyber threats posed additional challenges, highlighting the significance of complete insurance against both physical and digital risks to assets in the digital age

Solution

Conquer digital insurance woes, bolster cyber defenses, untangle regulations through collaboration, ride the tech wave through partnerships and innovation, and rebuild trust with data transparency and AI clarity. A fortified, innovative, and trustworthy future awaits

Implement robust cybersecurity measures

This includes spending money on data encryption, conducting frequent security audits, and providing staff with cybersecurity best practices training.

Establish a cooperative regulatory environment

To create transparent and uniform regulations for the digital insurance sector, regulators, insurers, and technology firms would need to be brought together.

Put innovation sandboxes into action

These are legislative “safe spaces” where insurance can evaluate new products and equipment without having to conform to established procedures for operation.

FAQs

What are the main problems associated with insurance?

The Top six hindrances Insurance Companies face today and How Leaders in the Industry Are Addressing Them

Economic Wellness Programs [EWP] can help with the increasing cost of healthcare, Regulatory Uncertainty, Changing Consumer Needs, Technology Disruption, Increasing Competition, and Changing Demographics.

Top risk faced in insurance in 2023?

Based on the 2023 survey, the top five industry risks are weather and natural disasters; regulatory or legislative developments; attacks or data breaches; delayed economic growth or slowdown; and the inability to draw or retain the best employees.

What are the 4 most significant insurances.?

The general agreement among insurance experts is that you should carry 4 forms of coverage: health, life, long-term disability, and auto insurance.